A Wi-Fi 6 licensing discussion can start with a large declared portfolio and still move quickly into a smaller number.

The patents may be declared against IEEE 802.11ax. The families may map to standard features. The portfolio may look broad enough to support a strong opening position.

The licensee’s next question changes the negotiation.

Which of those features are actually implemented in the products being licensed?

That question does not challenge the existence of the standard. It challenges the commercial exposure of the asserted portfolio. A patent covering a Wi-Fi 6 feature implemented across flagship smartphones, automotive systems, and IoT devices carries a different negotiating weight from one covering a feature that appears only selectively in low-power devices.

Declared essentiality starts the discussion. Implementation determines how much of the portfolio survives it. The full deployment-gap analysis behind this framework is available in a recorded session, mapping 5,000+ Wi-Fi 6 patents against certified products across smartphones, automotive, and IoT.

Register to get the webinar recording on: The Deployment Gap: Why Your Wi-Fi 6 Portfolio May Be Worth Less Than You Think

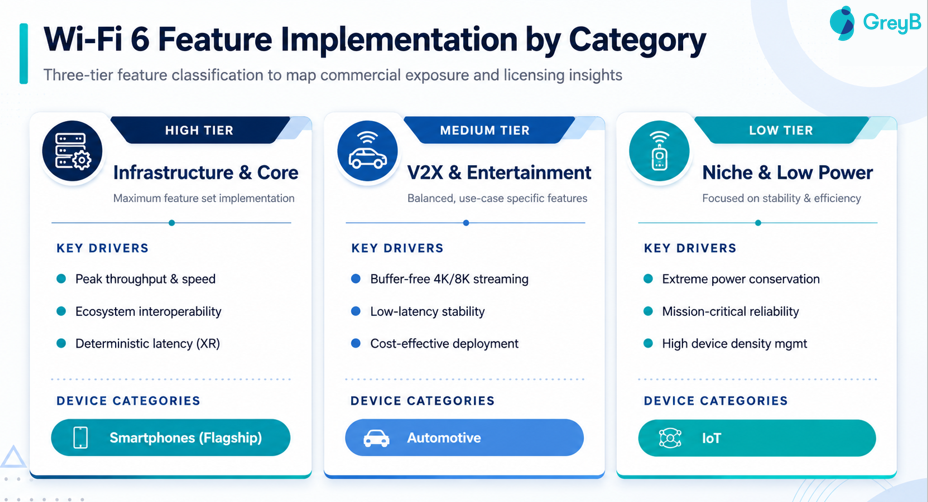

The same Wi-Fi 6 portfolio does not create the same exposure in every device category

The analysis mapped a 5K Wi-Fi 6 patent set across smartphones, automotive, and IoT using a high, medium, and low adoption tier framework. The tiers measure commercial implementation intensity, not technical sophistication.

That distinction matters.

High-tier features represent the commercial core of Wi-Fi 6. These are implemented at maximum intensity in infrastructure and core device environments, with smartphones as the strongest anchor category. Medium-tier features reflect balanced, use-case-specific implementation, especially around V2X and entertainment. Low-tier features reflect narrower deployment in systems built around power conservation, reliability, and device density.

A declared portfolio does not show this split. It treats the standard as a single licensing surface.

The implementation view breaks that surface into product-specific exposure. Smartphones, automotive systems, and IoT devices do not absorb Wi-Fi 6 features at the same rate or for the same reasons.

A smartphone needs throughput, speed, interoperability, and battery performance. Automotive Wi-Fi 6 deployment is more selective, tied to in-vehicle use cases and system design choices. IoT devices prioritize power, density, and reliability over the full feature intensity of a flagship phone.

The result is a licensing problem. The same asserted portfolio can be commercially strong against one category and weak against another.

Smartphone licensing still has the broadest high-tier exposure

Smartphones show why Wi-Fi 6 SEP owners still have leverage when the target category matches the implementation profile.

In the 5K patent set, 69.8% of mapped patents fall into high-adoption features for smartphones. Another 15.8% sits in medium adoption, while 14.4% maps to low adoption.

That distribution gives smartphone licensing a dense implementation base. Nearly seven out of ten mapped patents sit in features that the category already implements at high intensity. For a smartphone manufacturer, the declared portfolio is not merely a standard-alignment claim. A large portion of it sits inside the product’s implemented feature stack.

LDPC Rx/Tx shows the pattern. It is high in smartphones, but medium in automotive and IoT. The feature supports reliability and throughput, which makes it central in high-traffic smartphone environments. The same technical feature becomes more selective when the product has lighter traffic, different power constraints, or a narrower connectivity function.

The licensing implication is direct. A patent family covering LDPC does not have one uniform value across Wi-Fi 6. It has strong smartphone exposure and a more limited implementation argument in automotive and IoT.

A declared Wi-Fi 6 family does not carry the same commercial weight across device categories. The portfolio starts to change once you ask where the feature is actually deployed, not just where it is declared.

— Vishesh Saini, SEP Expert, GreyB

The 5,000-patent dataset referenced above, including the full high, medium, and low adoption tiers for every mapped feature, is broken down in this recorded session.

IoT turns broad Wi-Fi 6 assertions into a narrowing exercise

IoT produces the opposite profile.

In the same 5K patent set, only 39.1% of mapped patents fall into high-adoption features for IoT. Medium adoption accounts for 17.1%. Low adoption accounts for 43.8%.

That means the largest share of the Wi-Fi 6 patent set maps to features with low IoT implementation. For an IoT device manufacturer facing a broad Wi-Fi 6 licensing demand, this is the first reduction point. More than four out of ten mapped patents may cover features that the category does not implement at a meaningful scale.

This does not make those patents irrelevant in every setting. It makes them harder to use in a blanket IoT demand.

The reason is structural. IoT devices are not smaller smartphones. A sensor, smart home device, or industrial endpoint does not need every high-throughput Wi-Fi 6 capability to perform its function. Features such as MCS 10-11 Tx/Rx are high in smartphones, medium in automotive, and low in IoT. A-MPDU with A-MSDU is high in smartphones, medium in automotive, and low in IoT. Individual Target Wake Time is high in smartphones, low in automotive, and medium in IoT.

The implementation curve is not uniform. It follows the use case.

A smartphone licensing playbook, therefore, breaks down when applied to IoT. The asserted portfolio must be filtered by the features the IoT product actually deploys.

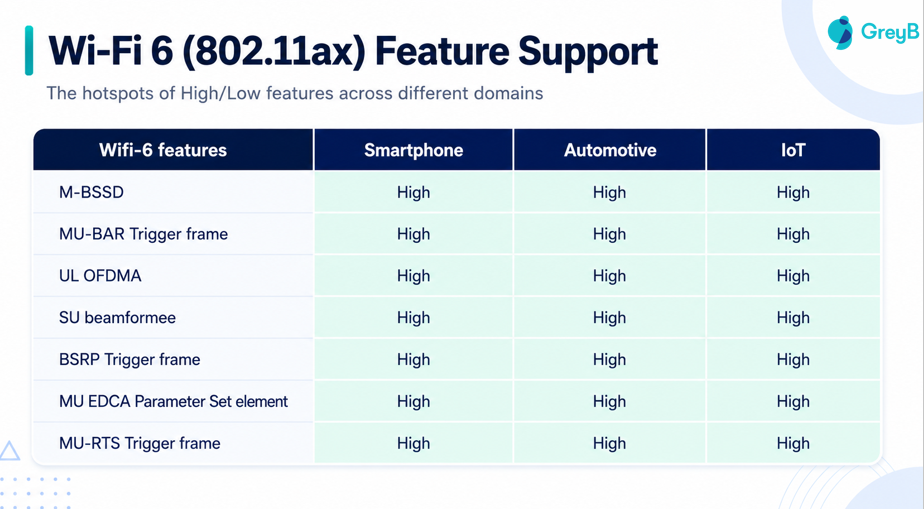

Seven features form the licensing core that survives across all three domains

Not every Wi-Fi 6 feature creates the same segmentation problem.

Seven features are high across smartphones, automotive, and IoT: M-BSSID, MU-BAR Trigger frame, UL OFDMA, SU beamformee, BSRP Trigger frame, MU EDCA Parameter Set element, and MU-RTS Trigger frame.

These features cover 1,981 patents in the 5K dataset. That is 39.1% of the mapped set.

This is the universal commercial core of Wi-Fi 6. Patents covering these features have the broadest licensing surface because all three device categories implement them at high intensity. They are the families most likely to survive an implementation-adjusted narrowing exercise.

The opposite group creates the licensee’s strongest filter. UL MU-MIMO, UL MU Control, Target Wake Time information frames, Broadcast Target Wake Time, Preamble Puncturing, Dynamic MU SMPS, and Extended sleep time are low across all three domains.

Low adoption doesn’t mean no future value. It means the present assertion needs more proof. A patent owner relying heavily on these features must show why the target product implements them, or why current low deployment understates the commercial trajectory.

That is a different negotiating position from the universal core.

Automotive has less middle ground than licensors may expect

Automotive sits between the smartphone and IoT profiles, but not evenly.

In the 5K patent distribution, automotive shows 59.8% high-tier concentration, 4.8% medium-tier concentration, and 35.4% low-tier concentration. The compressed medium tier matters because it shows that automotive adoption tends to be binary. A feature is either implemented because it fits the vehicle use case, or it falls out of the product’s commercial exposure.

That creates a sharper licensing test.

An automotive OEM is unlikely to accept a broad Wi-Fi 6 portfolio narrative if the asserted families map to features outside its deployed connectivity architecture. The relevant question is narrower. Does the vehicle system implement the feature covered by the asserted patent family?

If the answer is yes, the licensor has a stronger argument. If the answer is no, declared essentiality does not carry the same force.

This is where proportionality becomes practical. The implemented feature mix defines which parts of the portfolio can support the royalty discussion and which parts inflate the demand without strengthening it.

IoT is the main divergence driver in the Wi-Fi 6 portfolio value

The cross-domain split is not random.

The slide deck identifies IoT as the primary divergence driver. Out of 22 features with different tier rankings across domains, 19 have a lower tier in IoT.

That finding explains why broad Wi-Fi 6 licensing becomes unstable in connected-device markets. The standard may be common, but implementation is not. IoT pulls the portfolio away from smartphone assumptions because its product requirements are built around low power, reliability, and high device density.

This changes both sides of the table.

For licensors, IoT requires a scoped demand. The strongest opening position is not the total declared portfolio. It is the subset of families mapped to high and medium IoT features, with claim-level support for the products being licensed.

For licensees, IoT creates a credible reduction path. Families mapped to low-tier IoT features can be challenged early, especially when the product does not implement those capabilities at commercial scale.

IoT does not weaken Wi-Fi 6 licensing by default. It weakens Wi-Fi 6 licensing positions that were built for smartphones and then pointed at IoT without implementation filtering.

— Vishesh Saini, SEP Expert, GreyB

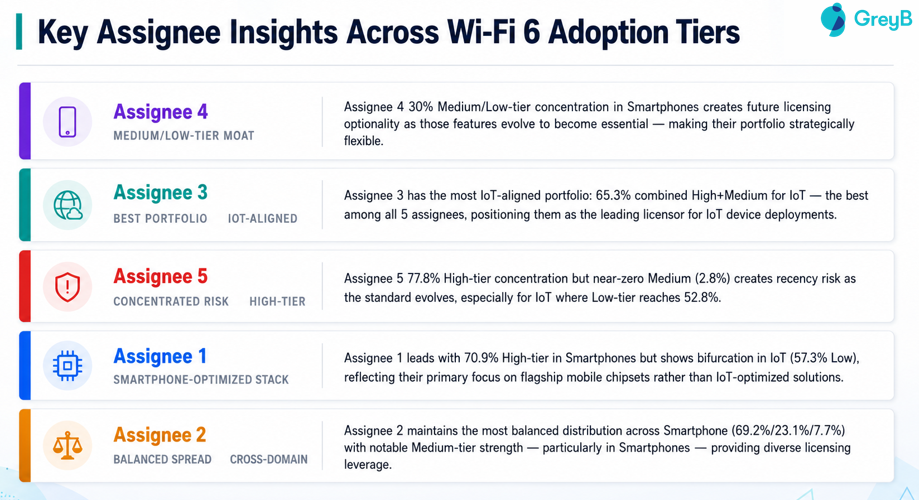

Assignee rankings change once deployment tiers are applied

A portfolio can look strong by declared count and still be misaligned with the target category.

The assignee-level analysis shows this clearly. Five Wi-Fi 6 assignees were mapped by high, medium, and low adoption tiers across smartphones, automotive, and IoT.

| Assignee | Smartphone | Automotive | IoT |

| Assignee 1 | 70.9% / 17.1% / 12% | 59.8% / 9.4% / 30.8% | 27.4% / 15.4% / 57.3% |

| Assignee 2 | 69.2% / 23.1% / 7.7% | 46.2% / 7.7% / 46.2% | 38.5% / 15.4% / 46.2% |

| Assignee 3 | 69.5% / 10.5% / 20% | 57.9% / 7.4% / 34.7% | 44.2% / 21.1% / 34.7% |

| Assignee 4 | 53% / 32.2% / 14.8% | 46.1% / 8.7% / 45.2% | 38.3% / 23.5% / 38.3% |

| Assignee 5 | 77.8% / 2.8% / 19.4% | 58.3% / 2.8% / 38.9% | 33.3% / 13.9% / 52.8% |

The table shows high, medium, and low-tier concentrations in that order.

Assignee 5has the strongest high-tier smartphone concentration at 77.8%. That gives it a strong current-market position in smartphone licensing. The same portfolio has only 2.8% medium-tier exposure in smartphones and 52.8% low-tier exposure in IoT. That creates recency risk as Wi-Fi 6 adoption evolves beyond today’s strongest smartphone features.

Assignee 3 has the best IoT alignment among the five. Its IoT portfolio has 44.2% high-tier and 21.1% medium-tier concentration, giving it a combined 65.3% high and medium share. That makes the portfolio more suitable for IoT licensing than a smartphone-heavy portfolio with a larger low-tier IoT share.

Assignee 4 presents a different profile. Its 53% high-tier smartphone concentration is the lowest among the five, but its 32.2% medium-tier smartphone concentration is the highest. That is not a weakness if those medium-tier features expand in commercial adoption. It gives the portfolio optionality as implementation shifts.

Assignee 1 is smartphone-optimized. It has 70.9% high-tier concentration in smartphones, but 57.3% low-tier concentration in IoT. Assignee 2 has a more balanced smartphone distribution, with 69.2% high, 23.1% medium, and 7.7% low, giving it more diversified licensing angles than a portfolio concentrated almost entirely in current high-tier features.

The ranking changes by target category. That is the point.

The anonymized view shows the direction of the analysis. The complete dataset shows the named assignees, feature-level mappings, and adoption-tier breakdowns behind each portfolio profile.

The strongest portfolio is the one already reduced to the implemented core

A declaration-led licensing demand gives the implementer the first move. The licensee can challenge essentiality, challenge implementation, and reduce the asserted set inside the room.

An implementation-adjusted demand performs that reduction before the negotiation begins.

That means leading with the families that map to high-adoption features in the target category. It means separating universal-core features from category-specific features. It means showing where the portfolio sits in smartphone, automotive, and IoT implementation profiles instead of presenting a single aggregate SEP count.

The economic effect is different. A licensee cannot reduce a portfolio in the same way when the licensor has already scoped it to the implemented feature set.

This also changes portfolio management. High-tier coverage supports current monetization. Medium-tier coverage supports future adoption scenarios. Low-tier coverage requires timing, patience, and a clearer view of which product categories may adopt those features later.

The question is no longer how many Wi-Fi 6 families a company owns. It is how many of those families are commercially usable against the products being licensed.

The portfolio owner who maps implementation first controls the scope of the discussion. The one who leads with declarations lets the other side decide which patents still matter.

– Vishesh, SEP Expert, GreyB

A Wi-Fi 6 licensing position that cannot answer these questions is exposed

Before a Wi-Fi 6 portfolio is asserted against a smartphone, automotive, or IoT implementer, the licensing team should be able to answer five questions:

- Which asserted families map to high, medium, and low adoption of Wi-Fi 6 features in the target device category?

- How much of the portfolio sits in the seven universal high-adoption features that cover 1,981 patents in the mapped dataset?

- Which families lose commercial force because the target product category implements the covered feature at low intensity?

- How does the assignee’s tier profile change across smartphones, automotive, and IoT?

- Which medium-tier features could move into higher adoption and change the portfolio’s future licensing leverage?

These questions follow the same sequence that a prepared implementer will use. They start with inventory, move to implementation, narrow the asserted set, compare category exposure, and identify future leverage.

Most Wi-Fi 6 portfolios have not been valued through this implementation-adjusted lens. The single most actionable output is a feature-level portfolio map that shows which declared families are commercially usable against each target device category.

This is the methodology covered in “The Deployment Gap: Why Your Wi-Fi 6 Portfolio May Be Worth Less Than You Think.” The recording includes the full master matrix, five mapped assignee profiles, and a live walkthrough of applying deployment data in negotiation.