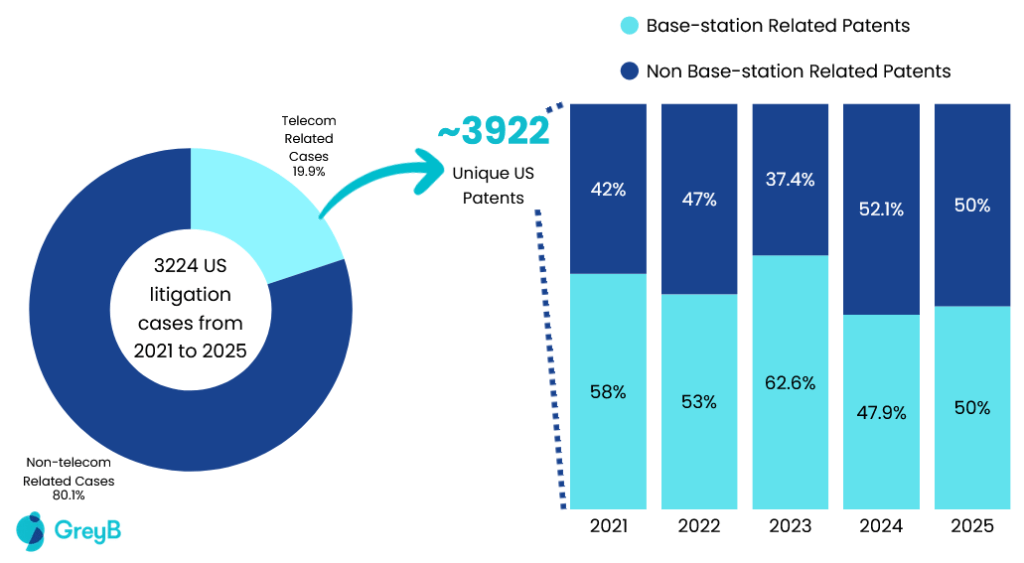

An analysis of approximately 3224 US litigation cases from 2021 to 2025 involved ~3922 unique US patents. A deeper dive into those patents revealed that base station-related patents account for 52% of all telecom litigation on the docket. The five most frequently named defendants across that period are AT&T, Samsung, Verizon, T-Mobile USA, and Ericsson.

Base station patent litigation is not a growing threat.

It has been the dominant reality in telecom IP for five consecutive years. The companies treating it as an emerging risk to monitor have already missed the first wave.

In 2024, Ericsson was named directly in a US antitrust case by Celerity IP, a non-practicing entity that had accumulated base station patents through secondary-market acquisitions.

In the same period, Malikie Innovations, the licensing subsidiary that acquired BlackBerry’s 32,000-strong patent portfolio for $200 million in 2023, launched enforcement campaigns against Xiaomi, Acer, and ASUSTek. Acer and ASUSTek settled. Xiaomi did not.

The question the above data raises is why, despite five years of sustained volume, most organizations in the assertion path have not recalibrated their exposure assessments to match it.

The answer sits in the patent acquisition market.

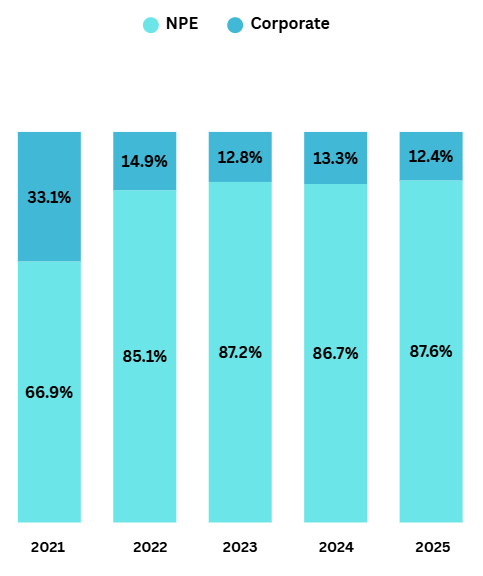

Sixty Percent of Base Station Patent Acquisition Volume Went to NPEs

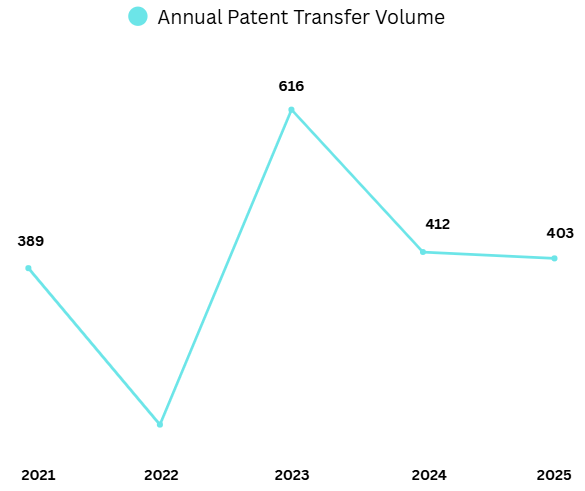

Between 2021 and 2025, over 1,900 patent families specifically related to base station technology changed hands. Non-practicing entities and licensing companies accounted for 58.5% of all purchases by industry category, approximately 1,162 families.

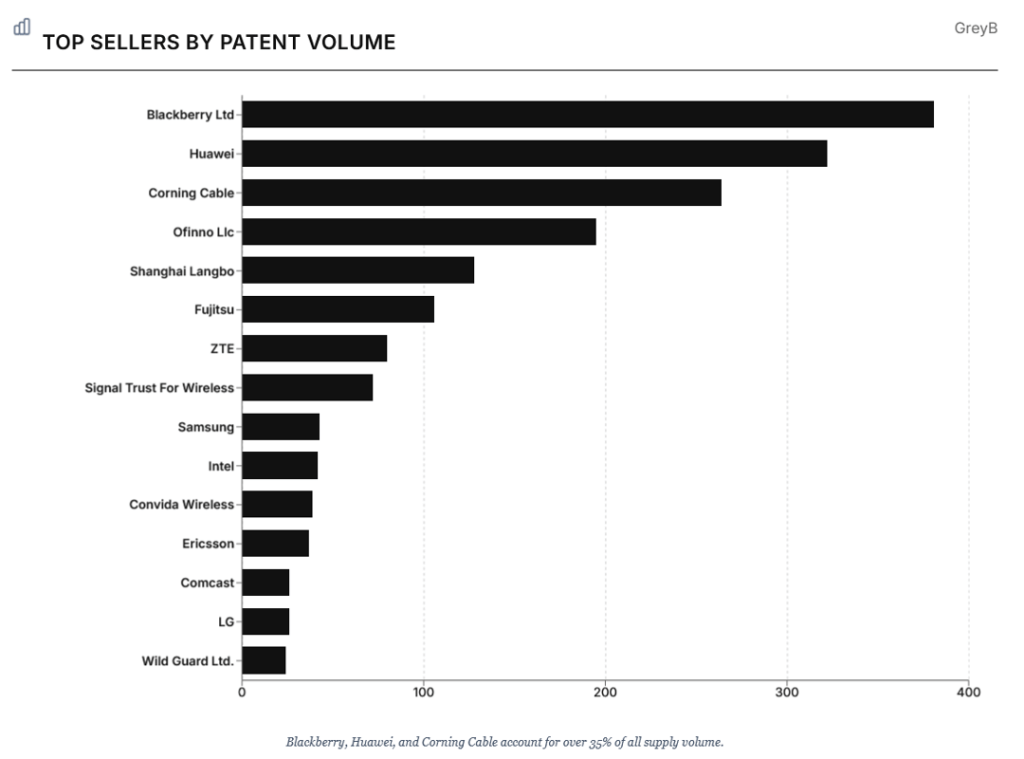

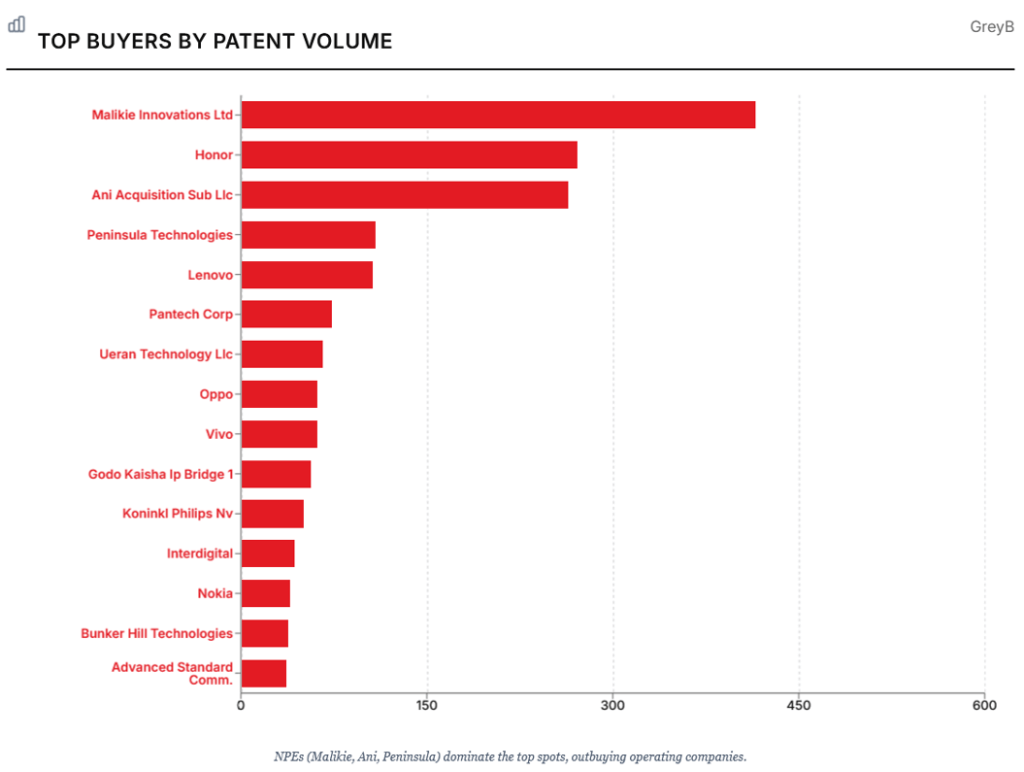

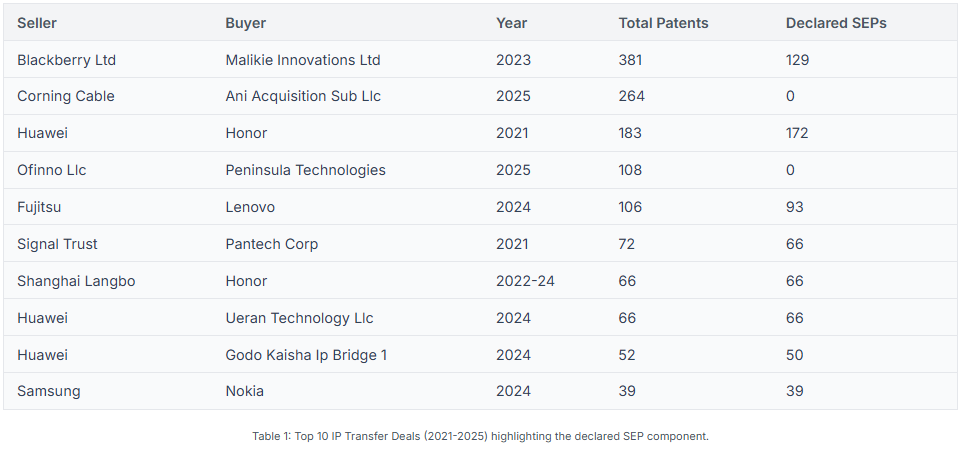

The three most active buyers over the entire period were Malikie Innovations (415 families), Ani Acquisition Sub LLC (264 families), and Peninsula Technologies LLC (108 families).

This connects the courtroom pattern to the ownership pattern. The patents driving base station exposure are not merely being litigated; they are also being concentrated in the hands of entities built around monetization.

SEP Status of the Acquired Patents

The next question is not only who is buying these assets, but what kind of patents they are buying.

A significant and growing share of the base station patents that have transferred to non-practicing entities carry no declared SEP status. They are implementation patents, covering how base station technology is built and operated, not what was contributed to a cellular standard. FRAND commitments do not apply to them. There is no established royalty benchmark to anchor a negotiation. There is no cross-licensing offset available to a defendant whose IP position is built entirely around declared SEPs. The licensing dispute that emerges from an implementation patent assertion starts from a blank sheet, and the blank sheet almost always favors the party holding the patent.

Also Read:

Recent transactions illustrate this clearly. The Huawei-to-Honor transfer in 2021 involved 183 patents, 172 of which were declared SEPs, a ratio of 94%. The strategic logic is transparent. Declared SEPs carry FRAND obligations but also come with an established licensing infrastructure and commercially recognized benchmarks. Honor acquired standard-essential leverage suited to cross-licensing negotiations with peers operating in the same FRAND-governed framework.

That transaction shows how SEP-heavy transfers fit within a known licensing framework. The contrast becomes sharper when the acquired portfolio falls outside that framework.

By contrast, the Corning-to-Ani Acquisition deal in 2025 involved hundreds of patents with no declared SEP status.

Every patent in that portfolio is an implementation patent. There is no FRAND framework governing their assertion, no established royalty rate to anchor negotiations, and no cross-licensing offset available to a defendant whose IP position is built solely on standard-essential patents. The Ofinno-to-Peninsula Technologies transfer in the same year moved 108 families, each with a declared SEP count of zero.

The consequence of that shift is already visible in recent filings.

When we see the consequences, we found that “Peninsula Technologies LLC” has filed cases, i.e., 2-25-cv-00386 (defendants – Dish Wireless, LLC d/b/a Boost Mobile, VOXX International Corp), 2-25-cv-00387 (defendants – Dish Wireless, LLC d/b/a Boost Mobile), 2-25-cv-01028 (Defendant – Chipotle Mexican Grill, Inc.) & 2-25-cv-01024 (Fortinet, Inc.).

The Policy Argument and the Asset Movement Are Pointing in the Same Direction

This base station patent acquisition is not happening in isolation. It is unfolding alongside a broader argument about where telecom licensing value should sit.

Alongside these transactions, a broader shift in thinking began surfacing at industry forums.

At IPBC Asia in 2025, licensing strategists from Xiaomi and Oppo surfaced a paper authored by Dr. John Gong, a Chinese economics professor. It argues that base station companies should bear significantly higher SEP licensing costs, effectively proposing a rebalancing of royalty flows away from handset manufacturers and toward the infrastructure layer. That debate has not been resolved.

“What is observable, however, is the timing. The companies most closely associated with advancing that argument have simultaneously been active in transferring base station-related patents to third-party entities. Policy advocacy for higher infrastructure-layer royalties and the parallel movement of base station assets into assertion vehicles are not, on the available evidence, unconnected developments. One provides the commercial rationale; the other builds the enforcement infrastructure to capture it.”

The combined effect is a repositioning of base station patents away from the standard-based licensing frameworks that have governed SEP disputes for two decades, toward assertion strategies in which fewer established rules apply, and negotiating outcomes are considerably less predictable. For the companies on the potential receiving end of those strategies, that shift, from FRAND-constrained SEP licensing to unconstrained implementation patent assertion, represents a categorically different risk profile than the one their current exposure assessments are built to address.

Once the market and policy context are clear, the next step is to look at the specific patents repeatedly used in litigation.

5 Most Frequently Used Base Station Patents In Litigation

Understanding which patents drive the highest litigation volume provides a practical lens on where assertion risk concentrates.

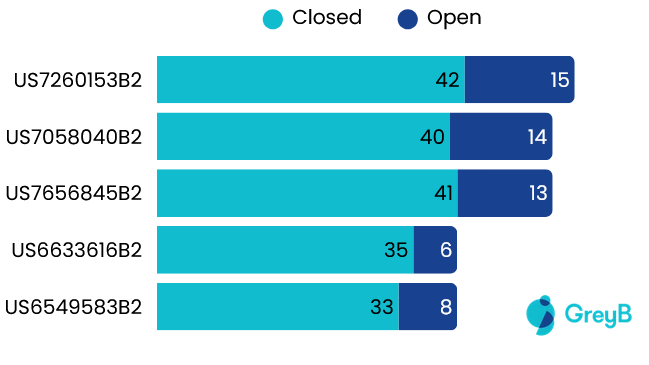

Cases by status of the top 5 most litigated patents

The five most-asserted base station patents span fundamental physical-layer technologies, all of which are currently held by Fleet Connect Solutions LLC. US7260153B2 (Fleet Connect Solutions LLC) pertains to SVD-based MIMO processing, including the calculation of singular values and pre-equalizer matrices, a core physical-layer algorithm used in MIMO base stations.

US7058040B2 (Fleet Connect Solutions LLC) and US7656845B2 (Fleet Connect Solutions LLC) focus on data transmission over overlapping media; the latter explicitly claims base station-side allocation functions relevant to radio resource management and scheduling.

US6633616B2(Fleet Connect Solutions LLC) describes a pilot phase error metric hardware block for OFDM receivers, directly relevant to base station hardware performance. US6549583B2 (Fleet Connect Solutions LLC) discloses a method of pilot phase error estimation, a fundamental PHY-layer signal processing function required for standard-compliant operation in LTE, 5G, and Wi-Fi systems.

Also Read:

From a portfolio perspective, in MIMO channel crosstalk parameter determination, companies such as Nxgen LLC, Sony, and Qualcomm hold a significant number of patents. In base-station scheduling, Huawei, Nokia, and Ericsson appear to have strong portfolios. In phase tracking using pilots, Qualcomm, Huawei, NTT, and Apple hold a substantial number of relevant patents.

Their current litigation status shows that these patents are not just historically important; they remain active enforcement assets.

Current litigation status of these patents

At present, these patents are involved in more than five active litigation cases.

The ongoing litigation involves companies that manufacture telematics devices, GPS tracking units, and IoT hardware that rely on cellular or wireless transmission, including CalAmp Corp., PowerFleet Inc., UAB Xirgo Global, Xirgo Holdings Inc., Xirgo Technologies LLC, Eroad Ltd., Coretex Ltd., and Masternaut Limited. The litigation also extends to vehicle manufacturers with built-in connected telematics and wireless transmission units, such as PACCAR Inc. and Rivian Automotive LLC.

In addition, companies manufacturing consumer technology devices, including cameras, dashcams, and audio equipment with integrated wireless transmitting units such as Wi-Fi, Bluetooth, or cellular connectivity, have also been litigated using these five patents. Examples include Bose Corp., Nikon Corp., OM Digital Solutions Corp., and Olympus Corp.

Taken together, the litigation data, reassignment activity, SEP-status split, and active case record all point to the same conclusion.

The Patents That Will Drive the Next Five Years of Base Station Litigation Are Already in NPE Hands

The companies that will face the next wave of base station assertions may never have considered themselves licensing targets. They do not manufacture handsets. They do not hold weak SEP positions. Some hold no SEP exposure at all. What they share is that their products implement base station technology, and the patents now consolidated in NPE hands cover implementation, not standardization.

A robust declared SEP portfolio offers no defense against a claim that sits entirely outside the standardization framework it was built to address.

The practical implication is not about litigation readiness. It is about timing. By the time a complaint is filed, the strategic options available to a defendant have already narrowed considerably. The transfer records that would have signaled the risk were publicly available months, sometimes years, earlier, visible to those systematically watching the secondary market, invisible to those who were not.

At this point, the questions that matter are specific.

- Which NPE currently holds patents that read on a specific product line?

- Which technology area within a company’s stack carries the highest concentration of NPE-owned implementation patents?

- Which of those patents have an AI-generated risk assessment already mapped to a specific product?

- If a new NPE has entered the base station space in the last quarter, which companies are in its immediate assertion path, and which products are at risk?

The GreyB NPE Risk Dashboard is built to answer those questions before they become urgent.

It tracks daily the patents acquired by NPEs post-2022, maps them to companies and specific products at potential risk, identifies the technology areas with the highest concentration of NPE ownership, and surfaces AI-generated risk assessments at the individual patent level. That is why the risk assessment has to begin before a complaint is filed.

Request a demo of the NPE Dashboard by filling out the form below.

Methodology:

The conclusions in this analysis are drawn from a structured, multi-stage examination of US patent litigation and secondary market transfer data spanning 2021 to 2025. The methodology is worth stating explicitly, because the credibility of the counterintuitive findings it produces depends entirely on the rigor with which the underlying dataset was constructed.

The starting point was a corpus of 3,224 litigation cases filed in the United States over the five-year period, encompassing approximately 16,919 patents involved across those proceedings. That dataset was not treated as a single body of telecom litigation. It was filtered in two distinct stages designed to isolate base station-specific exposure with a precision that broad litigation surveys do not typically achieve.

The first stage tagged every patent involved in those cases to determine whether it carried telecom relevance, separating the telecom-related docket from the broader patent litigation environment. That filter identified 19.9% of cases as telecom-related, establishing the universe from which base station exposure was then measured.

The second stage applied a more exacting standard. Each patent within the telecom-relevant cases was examined at the claim level, specifically, whether any independent claim disclosed a base station claim or described a method performed by a base station. Patents whose claims focused exclusively on the user equipment side were excluded. This is the methodological decision that most distinguishes this analysis from surface-level litigation reviews, which frequently conflate user equipment and base station claims within the same telecom category and consequently understate or mischaracterize where assertion risk actually concentrates.

The two-stage tagging process found that, on average across the five-year period, 52% of all telecom-related cases involved base station claims, a figure that holds consistently across each year of the dataset rather than being skewed by a single anomalous period.

Because NPEs were identified as the dominant plaintiff class within the base station litigation docket, the analysis was extended to incorporate patent reassignment data for the same five-year window. That reassignment dataset, covering over 1,900 base station patent families, provides the secondary market context that explains why litigation volume has remained structurally elevated and where the assertion pipeline for future enforcement campaigns currently stands.